The Redemption Panic: Why BDC Gates Aren’t Defaults

Non-traded BDCs are gating withdrawals again. Having already lost money on retail private credit once, here’s how I read the headlines — and the three things that would actually worry me.

The headlines vs. the data

Every few weeks in 2026 another headline lands: a giant private-credit fund “throttles withdrawals,” “gates investors,” “limits redemptions.” It reads like the early frames of a run. Apollo, Blackstone, Ares, Blue Owl — the biggest names in the asset class, all capping how much money investors can pull out.

The instinct is to assume the loans are going bad. That instinct is mostly wrong. A redemption gate is a statement about liquidity terms, not about whether borrowers are paying. Conflating the two is the single most common error I see in the coverage — and the one that would have cost me money if I’d acted on it.

A label-reading problem, in two directions

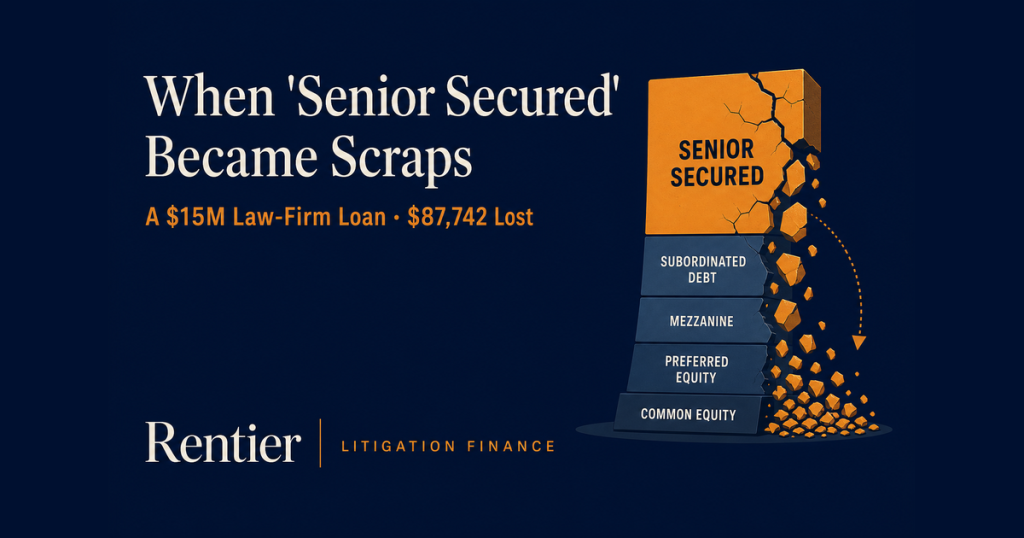

I’ll put my bias on the table. I lost money in retail private credit once, and it shaped how I read this. My YieldStreet “senior secured” law-firm financing deal put $250,000 into what the marketing called a senior secured position. Six and a half years later I had $162,258 back — a $87,742 loss, 0.65x MOIC. In the restructuring, the “senior” claim was subordinated behind a new lender and the “secured” collateral — a law firm’s pending cases — proved nearly impossible to realize.

Let me be honest about what that does and doesn’t tell you here: my loss is not evidence about Apollo or Blackstone. That was a single, illiquid, idiosyncratic SPV; these are large, diversified, professionally-managed funds. Different structure, different risk, different story. I’m not going to launder one into the other.

What the two do share is a single cognitive trap — and it’s worth seeing because it cuts in opposite directions. “Senior secured” was a reassuring label that hid more risk than it implied. “Redemption gate” is an alarming label that hides less. Same mistake — reading the word instead of the structure — producing opposite errors: I trusted a label I shouldn’t have; the market is now fearing one it shouldn’t. The discipline that would have saved me in 2018 is the same discipline that says don’t panic in 2026: ignore the label, read the structure. The rest of this post does exactly that.

The redemption wave is real

First, the facts. Q2 2026 redemption requests across the largest non-traded BDCs were genuinely elevated, and nearly every fund held the standard 5% quarterly cap:

| Fund | Q2 redemption requests | Quarterly cap |

|---|---|---|

| Apollo Debt Solutions (ADS) | 16.8% of NAV (~$2.4B) | 5% |

| Ares Strategic Income | 14.4% (2nd straight quarter) | 5% |

| Morgan Stanley North Haven | ~11.6% | 5% |

| Blackstone BCRED | ~10% | 5% |

| Blue Owl (two BDCs) | ~20% and ~40% | 5% |

Zoom out and the aggregate picture is the same: industry tender requests running roughly 12–15% of NAV, Q2 net flows tracking near -$3 billion, and new subscriptions softening faster than credit is deteriorating. Expect the redemption headlines to continue into Q3.

One detail the coverage mostly skips, and the one I find most telling: the selling skews offshore. At Apollo’s ADS, US onshore investors asked to redeem just 4.3% — while offshore requests hit 12.5%. That points to regional and structural dynamics in non-US wealth channels, not a US-retail verdict that the credit has gone bad.

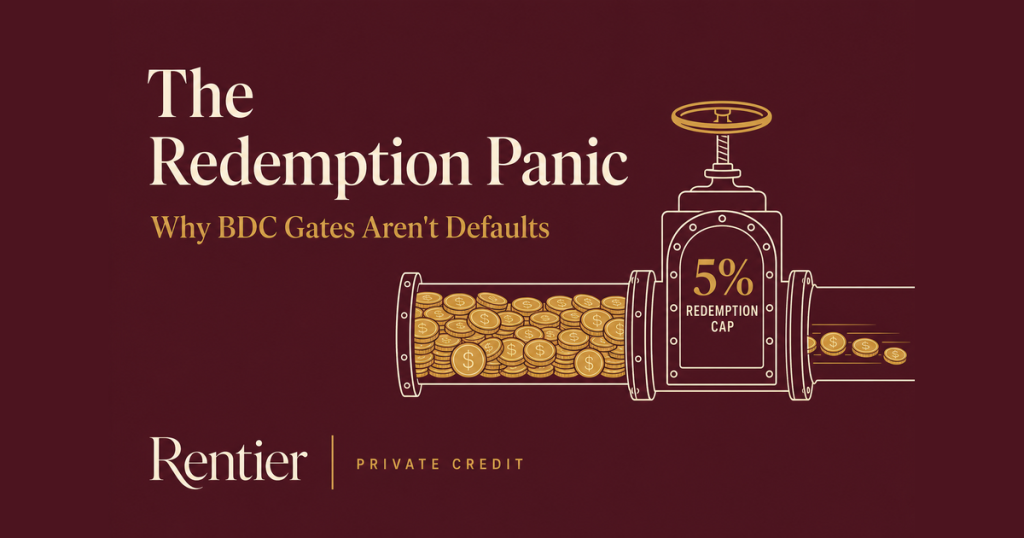

A gate is a feature, not a failure

Here’s what the word “gate” actually describes. Non-traded BDCs are semi-liquid by design: they hold illiquid private loans but offer limited quarterly liquidity, typically capped at 5% of NAV per quarter. That cap isn’t an emergency lever pulled in a crisis — it’s a contractual term written into the fund from day one, precisely so the manager is never forced to dump illiquid loans at fire-sale prices to meet withdrawals.

The structure has real shock absorbers:

- Short loan lives. Direct-lending loans average ~3-year lives, so a meaningful slice of the book naturally turns into cash every year without selling anything.

- Income generation. These portfolios throw off high-single-digit yields in cash, funding distributions and redemptions from coupon, not asset sales.

- Orderly queues. When requests exceed the cap, the excess rolls to future quarters. iCapital’s analysis notes that even a large redemption queue historically takes about a year to clear in an orderly way — not a fire sale.

A gate working is the system functioning as designed. The failure mode would be a fund forced to breach its own structure — selling loans at distressed marks to fund exits. That is not what’s happening.

Redemptions ≠ credit quality

This is the crux. Investors redeem for liquidity needs, sentiment, rebalancing, or because a hot narrative spooked them. None of those mean borrowers stopped paying. Outflows are a flows story; defaults are a credit story. The headlines describe the first and imply the second.

So to judge the actual health of the asset class, ignore the flow data and look at the credit data:

| Credit metric | Where it is now | What would worry me |

|---|---|---|

| Non-accruals | ~1.4%, mostly smaller borrowers; ~90% first-lien at ~40% LTV, so expected realized loss stays under the asset class’s ~1% long-run average | A climb toward 6% |

| PIK interest | ~14% of loans carry some PIK, but PIK is only ~7–8% of income (partial, not full); total PIK at the top 15 BDCs actually fell ~10% in Q1 | PIK rising as a share of income |

| Realized vs paper losses | Q1 marks were down ~1.1%, but mostly from spread widening — paper, not impairment | Paper markdowns converting to realized losses |

The PIK point deserves emphasis because it’s counterintuitive. Payment-in-kind — where interest is added to the loan balance instead of paid in cash — is the classic “extend and pretend” tell. But PIK falling, with managers favoring cash pay, is the opposite of distress. That’s de-risking, not deterioration.

The real fault line: software and AI

If there’s a genuine soft spot, it isn’t redemptions — it’s software. Technology and software borrowers are roughly 18–20% of direct-lending portfolios, and a lot of that was financed at 2020–22 peak valuations. Across the largest BDCs, software loan marks have slipped from about 99.5 to 97.5, while non-software credit stayed broadly stable. Funds with greater than 20% software exposure feel this most.

But “software” is not one thing, and this is where lazy analysis fails. The credit question per borrower is simple to state and hard to answer: is AI displacing this company’s product, or is the company deploying AI to entrench itself? Mission-critical enterprise software with deep integrations and high switching costs is a fundamentally different credit than a commoditized point-solution SaaS that a newer tool can leapfrog. A fund’s software percentage tells you almost nothing without that distinction.

The bull case: a lender-friendly reset

The flip side of the gloom is that conditions for new lending have rarely been better for disciplined managers. With some capital sidelined and competition thinner, new-issue yields are running around 9.5%, terms and covenants are tightening in lenders’ favor, and the gap between strong and weak managers is widening — exactly the environment where underwriting discipline gets paid.

That dispersion is the whole game. The asset class isn’t “good” or “bad” right now; it’s separating. Sector mix, vintage exposure, and PIK reliance are pulling the strong books away from the weak ones.

My diligence checklist: would I buy a non-traded BDC here?

So where does the “read the structure, not the label” discipline actually land me? I’m not rushing in — semi-liquid retail vehicles still carry the traps that burned me before: liquidity you think you have until you don’t, and fee layers that survive even when your returns don’t. But the redemption panic itself isn’t a reason to stay away. If I were underwriting an allocation, these are the three tripwires I’d actually watch:

- Non-accruals trending toward 6%. Below that, this is noise. Above it, the credit story becomes real.

- PIK rising as a share of income. Falling PIK is healthy; a sustained rise means borrowers can’t pay cash.

- Software paper marks turning into realized losses. Markdowns from spread widening reverse; realized losses don’t.

And the fund-level questions that actually matter: software exposure (and what kind), vintage concentration in 2020–22, the real cost of the liquidity I’m being sold, and — the one I’ll never skip again — what the security actually secures.

Bottom line

The non-traded BDC redemption wave is a sentiment-and-liquidity event, not a credit event — at least not yet. Gates are the structure working as designed, redemptions don’t measure credit quality, and the actual credit metrics (non-accruals ~1.4%, PIK falling, losses still on paper) are benign. The genuine risk lives in software, and the genuine opportunity lives in manager dispersion.

None of this makes retail private credit safe — my own $87,742 lesson says otherwise. But notice the symmetry: I lost money trusting a label that promised safety (“senior secured”), while the market is now fleeing a label that merely sounds dangerous (“gated”). Both errors trace to the same shortcut — reading the word instead of the structure. The thing to fear was never “redemption.” It’s the underwriting underneath, and the fine print on what “secured” actually means. Watch the tripwires, not the headlines.

Sources

- iCapital: BDC Redemptions — Looking Beyond the Gates

- iCapital: Looking Beyond the Redemptions II

- PitchBook: Apollo private credit BDC holds 5% redemption limit after 17% Q2 requests

- PitchBook: Blackstone’s BCRED holds 5% repurchase cap after Q2 withdrawal requests of 10%

- InvestmentNews: Apollo throttles withdrawals from $26B private credit fund

- Alternative Credit Investor: High redemption requests persist across BDCs

- PitchBook: Interest from PIK loans at BDCs dips amid concerns over credit quality, AI disruption

- Heron Finance: The State of Private Credit Benchmark Report (Q2 2026)

- Man Group: Private Credit, Software and AI — A Manual for Markets

- Lord Abbett: 2026 Midyear Outlook — Private Credit’s Lender-Friendly Reset

Commentary and personal experience — not investment, legal, or tax advice. Investing carries risk, including total loss of capital. Always do your own due diligence.