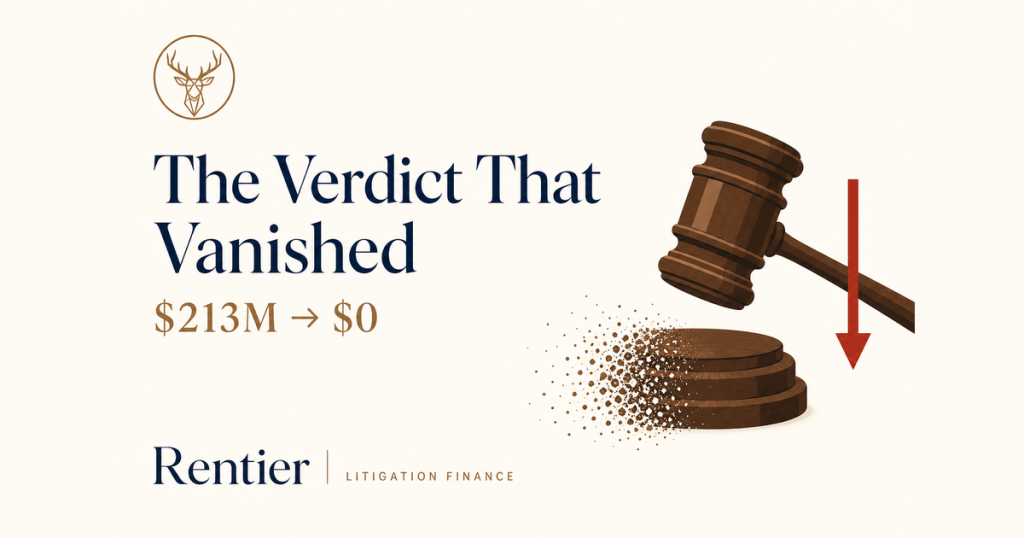

The Verdict That Vanished: Inside the “Take Care of Maya” Funding Fight

A $213M verdict became a $42M loan and a $60M insurance policy — then an appeals court erased it. What’s left is a fight over who gets paid when the headline number disappears.

I write about litigation finance as an investor, not a lawyer. For years I bought slices of individual funded cases through retail platforms — 42 of them, all in, for a whole-portfolio return of about 1.25% a year — and I lost real money on a note sold to me as “senior secured” that turned out to be neither. That era is over: I put new money into litigation finance funds now, not single cases. But the one lesson that outlived the retail experiment is this — the headline verdict is the least reliable number in the whole deal. Big awards get slashed on appeal, tangled up in collection, or reversed outright; the number that makes the news is the one least likely to become cash.

The “Take Care of Maya” case is that lesson playing out in public, on a famous file, in real time — and it comes with a second act that’s honestly just fascinating to watch from the outside. Once the headline money vanished, everyone who had bet on it started fighting over what was left.

The headline everyone remembers

Maya Kowalski’s story became a 2023 Netflix documentary, Take Care of Maya. In November 2023, a Florida jury found that Johns Hopkins All Children’s Hospital had falsely imprisoned Maya as a 10-year-old and that its conduct contributed to her mother Beata’s suicide. The award: about $261 million, later trimmed by the trial judge to roughly $213 million. It was the kind of number that makes headlines — and, it turns out, the kind that attracts financing.

The money built on the headline

A $213M judgment on appeal is not $213M in the bank. It’s a claim — contingent, years from final, and reversible. But it can be borrowed against. After the 2023 verdict, the Kowalskis took roughly $42 million as an advance from HPS Investment Partners, a large private-credit manager (acquired by BlackRock in 2025). To secure that advance, they bought a $60 million judgment preservation insurance (JPI) policy from Ambridge Group, brokered by Willis Towers Watson — the same species of instrument I wrote about in the patent context, designed to backstop a verdict that’s been won but not yet collected.

The redacted credit agreement, surfaced in court filings and reported by Bloomberg Law, shows the structure funders actually build. The family kept “sole, final, and unconditional” control of the appeal, retrial, and settlement — but not really. They can’t settle in a way that “adversely affects the interests of the lenders,” must keep HPS informed of every development, share draft filings, and give notice of settlement offers. They can be put in default if they settle against the lender’s interest or swap attorneys without HPS’s consent. Control, with a lender’s hand on the wheel.

Then the verdict evaporated

On October 29, 2025, Florida’s Second District Court of Appeal reversed the entire judgment. The court held that the trial had improperly blurred the hospital’s statutory good-faith immunity for reporting suspected child abuse, and sent the case back for a new trial on a narrowed set of claims — with no punitive damages available. The retrial is set for March 2027. As of today, the $213M is $0 until (and unless) a second jury says otherwise.

That is the whole point in a single move. The verdict was the foundation the loan and the insurance were built on. Pull the foundation and the structure above it doesn’t disappear — it just gets very complicated. The JPI policy exists precisely for this moment; whether and how it responds to a reversal-and-retrial (rather than a clean, final loss) is exactly the fine print that matters.

Now the fight is over the leftovers

With the verdict gone, the sharpest dispute isn’t the family versus the hospital — it’s the family versus their former lawyers. The Kowalskis are trying to stop their prior firm, AndersonGlenn LLP, from collecting a fee of nearly $10 million out of the HPS loan proceeds. In filings, they allege the attorneys didn’t properly explain the advance’s costs, fees, interest, and case-control restrictions; that a new fee agreement was presented to Maya shortly after she turned 18, while she was emotionally vulnerable; and that the fee terms exceeded Florida Bar limits and may have required court approval. They also say the lawyers took on roles beyond counsel — tied to collateral, account control, and administering the transaction itself.

These are allegations, not findings. The Andersons deny wrongdoing, and none of it has been tested at trial. But notice what the fight is about: not the merits of Maya’s case, but the mechanics of the money layered on top of it — the loan, the fees, the control terms, and the order in which people get paid.

What this actually shows

Strip away the documentary and the sympathetic facts, and this is a clinic in the structural risks that decide litigation-finance outcomes:

- The headline verdict is a marketing number, not a bank balance. $261M → $213M → $0-pending-retrial, in about 24 months. Everything financial downstream of it inherited that fragility.

- “Control” is a negotiated fiction. The claimant nominally ran the case but couldn’t settle freely or change lawyers without the lender’s sign-off. Read the covenants, not the cover page.

- JPI is the backstop everyone leans on and few stress-test. A $60M policy is only as good as how it treats a reversal-and-remand. The instrument gets bought on the assumption verdicts hold; the interesting cases are the ones where they don’t.

- The fee-and-repayment waterfall is where value really gets decided. When the pie shrinks, the fight moves to who stands where in line — lender, lawyers, then the claimant. That order matters more than the verdict’s size.

Where I land

I have no stake in this case, I’m reading public and partly-redacted filings, and the family’s allegations are unproven — so I hold the specifics loosely. It’s also entirely possible the insurance does its job and everyone lands roughly whole; that is what a JPI policy is for.

And that distance is the point for someone like me. I don’t underwrite deals like this — I don’t pick cases or read credit agreements for a living — and that’s exactly why my litigation finance money sits in funds. Untangling reversal risk, control covenants, insurance triggers, and the payment waterfall is specialist work I’d rather pay for than fumble. The Kowalski file is a tidy, public illustration of the mess I’ve handed off — and, read in reverse, a checklist of what I’d want the fund managers I’ve trusted to be worrying about: what happens on reversal, who really controls a settlement, where the lender and the lawyers sit in the waterfall, and exactly what the insurance pays, and when.

Beyond that, I’ll admit the plain appeal of the spectacle. The verdict was the story everyone tuned in for; the financing is the story that outlived it — a $42M loan, a $60M policy, and a nearly $10M fee fight now orbiting a number that no longer exists. It’s a useful reminder that in this asset class, the figure in the headline is the one I trust least, and the real money always moves in the fine print underneath it.

Sources

- “BlackRock Subsidiary’s Deal Revealed in ‘Take Care of Maya’ Case,” Bloomberg Law (2026) — redacted HPS Investment Partners credit agreement; ~$42M advance; $60M Ambridge Group JPI policy brokered by Willis Towers Watson; settlement/control covenants; ~$10M AndersonGlenn fee dispute. Jack Kowalski v. Johns Hopkins All Children’s Hospital, Fla. Cir. Ct. 2018-CA-005321-NC.

- “Family from ‘Take Care of Maya’ documentary accuses attorneys of fraud, financial misconduct,” WUSF (June 22, 2026) — ~$42.1M advanced-funding transaction; allegations re: fees, disclosures, and a post-18 fee agreement; the Andersons deny; family now represented by Childers Law.

- “Appeals court reverses judgment in ‘Take Care of Maya’ case,” WUSF / USA Today (Oct 29–31, 2025) — Fla. Second DCA reverses the ~$213M verdict on good-faith-immunity grounds; new trial (no punitive damages) set for March 2027.

Commentary and personal experience — not investment, legal, or tax advice. Investing carries risk, including total loss of capital. Always do your own due diligence.