42 Cases, 8 Investors, One Platform’s Collapse

How my investor group barely broke even on a litigation finance crowdfunding platform

The Bottom Line

My investor group put $2.3 million into 42 commercial litigation cases on LexShares from 2017-2020.

We barely broke even.

| Total Invested | $2,331,000 |

| Members | 8 |

| Cases | 42 |

| Record | 20 wins, 15 losses, 7 pending |

| IRR | 1.25% |

| Resolved MOIC | 1.05x |

On resolved cases, the group got back $1.05 for every dollar invested — barely positive after 7+ years. The final resolution of Passport Patent in January 2026 (1.84x) pushed several members from underwater to breakeven.

My Portfolio

I invested $1M of the group’s $2.3M — about 43% of the total, the core of my all-in bet on litigation finance. My results were better than the group average, but that’s mostly luck. We all stopped investing after Q1 2020. Some members concentrated heavily in cases that went badly — that’s the real difference, not timing.

| My Portfolio | Group Total | |

|---|---|---|

| Invested | $1,000,000 | $2,331,000 |

| Cases | 17 | 42 |

| Record | 9W-4L-4P | 20W-15L-7P |

| IRR | 4.98% | 1.25% |

Wins (9 cases, $420K invested → $699K returned)

| Case | Invested | Returned | MOIC |

|---|---|---|---|

| Toy Licensing | $25,000 | $64,135 | 2.57x |

| Passport Patent | $25,000 | $45,897 | 1.84x |

| NFL Fraud | $75,000 | $134,295 | 1.79x |

| Trade Secrets | $150,000 | $263,269 | 1.76x |

| Roundup | $25,000 | $42,399 | 1.70x |

| Medical Finance Fraud | $30,000 | $50,703 | 1.69x |

| Fuel Injection Patent | $30,000 | $33,710 | 1.12x |

| Trademark | $50,000 | $54,970 | 1.10x |

| Software Contract | $10,000 | $10,000 | 1.00x |

Losses (4 cases, $350K invested → $150K returned)

| Case | Invested | Returned | What Happened |

|---|---|---|---|

| Transit Lease | $82,500 | $0 | Rejected $5M settlement, lost at trial |

| Commercial Lease | $50,000 | $0 | Lost at trial, lawyer withdrew, appeal dismissed |

| Counterfeit Equipment | $47,500 | $0 | Spoliation sanctions |

| Knights of Columbus | $170,000 | $149,937 | Won trial, but $500K verdict vs $100M claim |

Performance by Vintage

| Year | Record (W-L-P) | IRR | Notes |

|---|---|---|---|

| 2017 | 5-4-2 | -2.81% | Early deals, mixed results |

| 2018 | 6-3-3 | 4.68% | Best vintage |

| 2019 | 6-8-2 | 0.75% | More losses than wins, but late resolutions helped |

| 2020 | 3-0-0 | 17.48% | Small sample, all resolved positive |

2019 had 8 losses vs only 6 wins. Late-resolving cases like Passport Patent (1.84x) pulled the vintage from negative to barely positive.

What Went Wrong

LexShares was a crowdfunding platform for individual litigation cases. They also launched pooled funds (Marketplace Fund I and II). Our group invested in individual cases — but the platform and funds shared the same problems.

To understand how badly LexShares underperformed, compare our results to sophisticated funders:

| Metric | LexShares (Our Group) | Sophisticated Funder Standard |

|---|---|---|

| Success Rate | 57% (20W / 35 resolved) | 80-92% |

| Gross MOIC (resolved) | 1.05x | 1.8-2.5x |

| Acceptance Rate | Unknown (appeared high) | <5% |

| Net IRR | 1.25% | >25% target |

Benchmarks: One middle-market funder reported 92% success rate and 1.8x MOIC on realized investments, funding just 3% of cases reviewed. Burford Capital’s concluded investments, inception through 2024, show a 26% IRR and an 87% ROIC — roughly 1.9x MOIC — across $3.3B of realizations.

LexShares failed on nearly every dimension.

Wrong Expertise at the Top

LexShares was founded in 2014 by Jay Greenberg and Max Volsky, with Volsky as Chief Investment Officer. The problem: Volsky’s deep track record was in consumer litigation finance, not commercial.

He was a genuine pioneer of the field — he’d overseen more than 10,000 legal-claim investments since 1999 and authored one of the first books on litigation finance. But a five-figure investment count is a consumer-volume signal: it comes from lawsuit advances and pre-settlement funding, where claims are numerous and settlement ranges predictable. Commercial litigation is the opposite — low-volume, high-variance, idiosyncratic.

Consumer and commercial litigation require fundamentally different underwriting:

- Consumer: High volume, predictable settlement ranges, insurance company defendants with settlement incentives

- Commercial: Low volume, highly variable outcomes, well-resourced corporate defendants with no routine settlement incentive — they settle only when the cost-benefit favors it

Applying consumer litigation heuristics to commercial cases led to systematic overvaluation.

Weak Case Selection

LexShares funded cases that institutional funders would reject:

- Distressed plaintiffs: The Commercial Lease case involved a landlord whose bank was foreclosing on his building while he sued his tenant

- Uncollectable defendants: In April 2020, after oil prices collapsed, LexShares offered a deal with an energy industry defendant whose financials looked terrible. I passed. They funded it anyway.

- Government defendants: Multiple cases against entities with no settlement pressure and willingness to fight indefinitely

- Irrational plaintiffs: The Transit Lease plaintiff rejected a $5M settlement offer and lost everything at trial

Sophisticated funders evaluate three distinct risks: liability (will the plaintiff win?), damages (how much?), and collectability (can the defendant pay?). LexShares focused almost exclusively on liability.

Overvalued Settlements

Even when LexShares picked winners, the returns were underwhelming:

- No 3x returns — the best was Toy Licensing at 2.57x

- Wins clustered at 1.5-2x — NFL Fraud 1.79x, Trade Secrets 1.76x, Roundup 1.70x

- Many “wins” barely profitable — Trademark 1.10x, Fuel Injection Patent 1.12x, Software Contract 1.00x

Plaintiffs frequently settled for far less than projected, then negotiated with LexShares to accept reduced returns. When your best outcome is 2.57x and most wins cluster at 1.5-1.8x, you need a near-perfect win rate to break even. Sophisticated funders structure deals for 3.5x multiples to build cushion for losses and time. LexShares’ return distribution left no buffer.

No Time for Retail Due Diligence

Once LexShares published a deal on the platform, it filled in under an hour. By the time I got access, read the summary, and started paperwork, one deal was already full. Retail investors had no time to conduct independent due diligence — you either invested blind or missed the deal entirely.

Declining Win Rate

In December 2017, LexShares reported 10 wins out of 11 resolved (~90%) and expected 75% going forward. Then they stopped releasing stats. By early 2020, only 2 of the last 9 resolved cases netted a profit — 4 were total losses.

Fund-Specific Problems

The pooled funds had additional issues:

- Deal-level carry: They calculated carried interest on each individual case, not at the fund level. Fund I reported -7% IRR in 2024 (now improved to ~4% on resolved cases as of Q3 2025) — but still collected carry on winners throughout. Standard fund-level carry would net winners against losers; deal-level carry meant LexShares collected on every winning case regardless of overall fund performance. Industry standard: 20% carry subject to 8% preferred return with 100% GP catch-up, calculated at the fund level.

- Cash drag from 100% upfront capital calls: Fund I called all committed capital on day one, then took 2+ years to deploy it — so investor cash sat idle in the fund instead of staying productive until it was needed. (Charging the management fee on committed capital during the investment period is itself standard practice; the problem here was calling everything upfront rather than as deals closed.) Investors complained as early as 2019. Sophisticated funds call capital just-in-time, tranched against deployment, so uncalled commitments keep working for the investor.

- Fee creep: Carried interest rose from 20% to 25% on the pooled funds (Fund I to Fund II) — and from 20% to 30% on direct case investments.

- Inflated IRR reporting: LexShares calculated IRR from the date of fund disbursement to plaintiffs, not the date of capital commitment. With 3-4 weeks of lag, this inflated their reported numbers. They also never provided MOIC — only IRR.

- Inflated returns: When Fund II launched in June 2020, they reported 52% median IRR and 69% win rate. Our group caught them inflating return multiples in the pitch deck — stated vs actual returns differed by 0.1-0.2x per case. The win rate dropped to 63% within a week of launch after a case resolved.

- Gross vs Net: More recently, investor letters started reporting gross IRR and MOIC rather than net returns — the numbers investors actually receive after fees. Another way to make performance look better than reality.

Early negative returns aren’t unusual in litigation finance — the J-curve effect (management fees charged before investments resolve) can show negative IRR even when underlying investments are performing. But LexShares’ problem wasn’t timing. The underlying investments were weak.

Track Record Opacity

LexShares refused to provide detailed track record data until each fund opened — convenient timing that prevented proper due diligence. When investors repeatedly asked for case-level statistics in 2018-2019, the company deflected, saying historical data would only be available when the next fund launched. This forced investors to either (1) wait indefinitely, (2) invest blind in individual deals, or (3) trust the curated statistics LexShares selectively released.

When Fund II launched in June 2020, our group evaluated it and passed. They fixed the capital call issue (10% upfront instead of 100%), but refused to change the deal-level carry structure. We stopped investing after Q1 2020.

What’s Left

I still have 4 cases pending ($230K invested). The group has 7.

| Case | Invested | Prob. | Status |

|---|---|---|---|

| Bovine Pharma | $75K | 65-75% | Hearing Jan 12-19, 2026 |

| Surveillance Patent | $100K | 60-70% | All 7 IPRs denied, patent validated July 2025 |

| ICSID Arbitration | $50K | 20-30% | Hearing Sept 2026; claimant bankrupt |

| Tribal Contract | $5K | 25-35% | 8 years of jurisdictional battles; got $1.8K back |

Bovine Pharma ($75K → ~$233K, Q2-Q3 2026): Hearing Jan 12-19, 2026 after 11 years of litigation. Product works (clinical trials proved efficacy in 2023), breaches are documented. Binding arbitration means no appeals — decision expected within months.

Surveillance Patent ($100K → ~$340K, Late 2026-2027): Survived every validity challenge — 7 IPR petitions denied and claims 1–10 of the ’980 patent twice confirmed in USPTO reexams (latest July 2025). After a long stay, the court has resumed proceedings for a limited portion of the case and ordered supplemental briefing on the pending partial summary judgment motion, with deadlines running through early 2026. Other parts of the case remain stayed. Strong on liability; damages are the question.

ICSID Arbitration ($50K → ~$250K, 2027-2029): The riskiest case. First claim dismissed because wrong party filed. Claimant is bankrupt. But insurers providing $2M security suggests the lawyers see merit. Hearing September 2026.

Tribal Contract ($5K → ~$17K, 2028+): An 8-year jurisdictional nightmare that just reset. At least I got 36% back ($1.8K) from a sanctions award.

Outlook

Platform: Effectively dead. In August 2024, LexShares cancelled Fund III and laid off most staff, entering “harvest mode.” Fund I has now distributed ~80% of committed capital, with 68% of deployed capital fully resolved and 32% still outstanding. The resolved portion is tracking at just under 4% net IRR — a significant improvement from the -7% reported in 2024, though still a poor outcome after 8+ years. In December 2025, the company settled a lawsuit with former CEO Cayse Llorens.

My portfolio: $849K already returned on $1M invested. If Bovine Pharma comes through (65-75% likely), I end up around 1.15-1.2x MOIC. Add Surveillance Patent and it could hit 1.4-1.5x. Not the 2-3x originally projected, but not a disaster — and in the context of my broader net worth, a meaningful concentration that quietly underperformed for the better part of a decade.

Group: The remaining 7 cases could push final returns meaningfully higher — but even in the best case, 7+ years of illiquidity for single-digit returns is a poor outcome.

My Share of the Blame

It would be easy to make this entirely LexShares’ fault. It isn’t. I chose the platform, funded 17 cases across three years, and most of the red flags I catalogued above were visible in real time — the acceptance rate that looked suspiciously high, the deals that filled in under an hour with no room for diligence, the company that stopped releasing stats in 2018 and deflected every request for case-level data. I noted those things and kept wiring money anyway, because each individual deal read well and the fear of missing the next one was louder than the pattern forming underneath. I did say no once — the April 2020 energy-defendant case — and I was right. So the problem wasn’t that I couldn’t see it; it’s that I didn’t act on what I saw, often enough.

The cleaner way to put it: I outsourced underwriting to a counterparty whose incentives I’d never examined, and let “the deal looks good” stand in for “the underwriter is good.” That’s the same mistake in a different costume from my “senior secured” YieldStreet loss — trusting the label on the deal instead of the structure and the incentives behind it. Two platforms, one root cause, and the tuition wasn’t cheap.

The Lesson

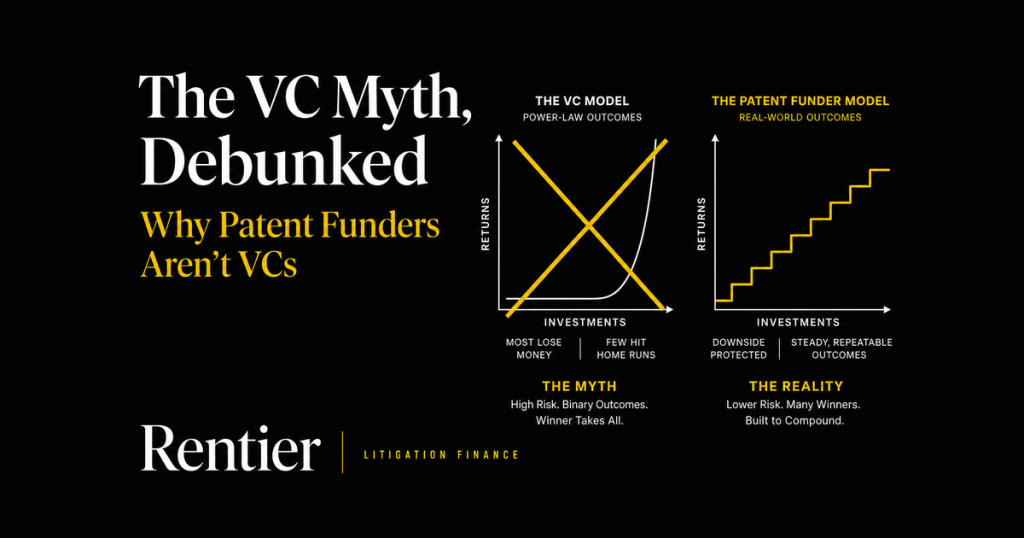

Litigation finance as an asset class works. Institutional funders (Burford, Longford, Parabellum) target 25%+ net IRR with proper underwriting. Sophisticated funders accept <5% of cases reviewed, staff teams with former commercial litigators and public company executives, structure deals for 3.5x multiples with 10:1 recovery-to-funding ratios, and align fees at the fund level. The gap isn’t the asset class; it’s the underwriter — I’ve since worked through why the biggest funders aren’t running spray-and-pray and what disciplined, platform-scale access actually demands, both of which describe the opposite of what I bought here.

LexShares failed systematically. The 1.25% group IRR and platform collapse weren’t bad luck — they were predictable consequences of consumer litigation expertise applied to commercial cases, weak case selection, and misaligned incentives. The deal-level carry (which increased from 20% to 30% on direct investments, and 20% to 25% on pooled funds) let managers profit even when investors lost money.

The middle market opportunity was real. LexShares operated in the $0.5-4M investment segment — claims seeking $5-40M in damages. Most large funders (Burford, Omni Bridgeway) focus on cases requiring $4M+ funding, leaving this segment underserved. With proper underwriting, this should have been an advantage. LexShares squandered it.

And the ground is shifting under the asset class. Since I started in 2017, litigation finance has picked up a regulatory risk it didn’t used to carry: states are moving on funder disclosure, and North Carolina went all the way to an outright ban. Venue and disclosure regime are now underwriting inputs alongside the merits — one more reason any retail exposure belongs with a disciplined fund that can navigate it, not a single case picked off a website.

Learning about litigation finance through LexShares was valuable. Trusting them as the underwriter was the expensive mistake.

Sources: LexShares case updates through Jan 2026; public court filings/PACER docket activity for pending cases through Dec 2025; Fund I data from investor reports (Q3 2025); investor group tracking data. Benchmarks from middle-market funder investor presentation (2024), Burford Capital annual reports.

Commentary and personal experience — not investment, legal, or tax advice. Investing carries risk, including total loss of capital. Always do your own due diligence.